Monomaterial PET vs Monomaterial PP: Which One Fits Your Cosmetic Packaging?

With the EU Packaging and Packaging Waste Regulation (PPWR) becoming applicable on 12 August 2026, "design for recycling" has shifted from a sustainability talking point to a compliance requirement. Mono-material construction (where the bottle, cap, and ideally the label are all made of the same resin) is one of the most reliable routes to a packaging design that survives the new recyclability classes.

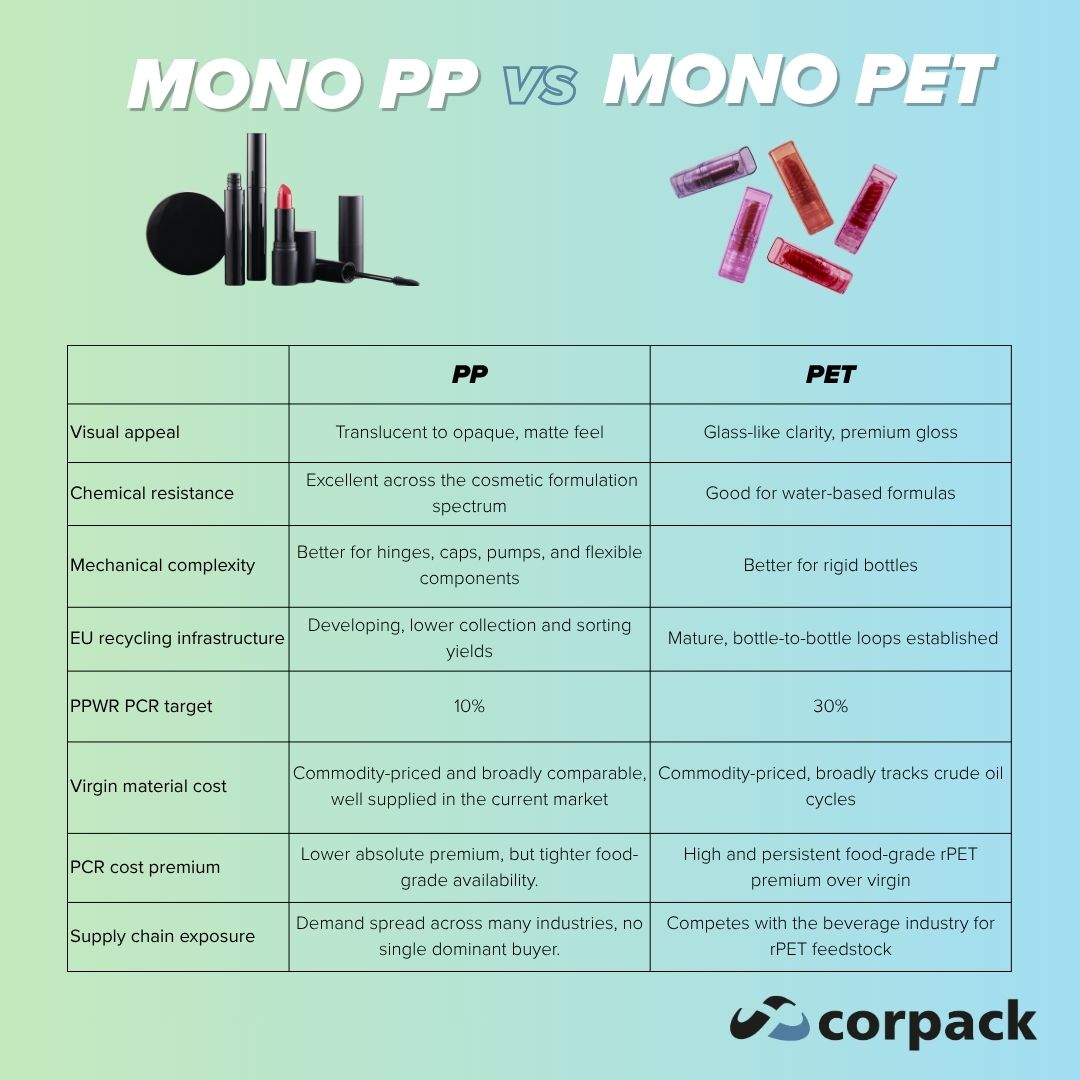

But "mono-material" is not a single choice. The two dominant options for cosmetic packaging are PET and PP, and they behave very differently. The decision shapes everything from your product's shelf appeal to your PCR content strategy, and increasingly to your procurement position. Here is what brands need to know before specifying one over the other.

Why Mono-material Matters Now

Under the PPWR, packaging will be graded into recyclability performance classes from A to E, with Class A reserved for packaging that can be recycled with 95% or higher efficiency. Pure mono-material constructions are the cleanest route to the top grades. Composite packaging (a PET bottle with a metal-coated cap, for example, or a multi-layer laminate) will struggle to clear the threshold. From 1 January 2030, only packaging graded A, B or C may be placed on the EU market, which means anything in Class D or E is excluded. The bar then rises again in 2038, when Class C is phased out and only A and B remain.

The regulation also introduces minimum PCR content targets. For contact-sensitive cosmetic packaging, the differential between PET and PP is significant: 30% PCR for PET by 2030, versus 10% for non-PET contact-sensitive packaging including PP. That gap reflects the maturity of the two recycling streams, and it has direct cost and sourcing implications.

PET at a Glance

Polyethylene terephthalate (PET) is the workhorse of transparent bottle packaging. Its molecular structure produces a glass-like clarity that PP cannot match, which is why PET dominates skincare bottles, toners, body lotions, and serums where the brand wants the formula visible on shelf.

Strengths:

- High clarity and gloss for premium shelf appeal without glass

- Good barrier properties against moisture and oxygen

- Mature recycling infrastructure across the EU, with established bottle-to-bottle loops

- Wide availability of food-grade PCR (rPET), often at 30–100% content

- Higher density (~1.38 g/cm³), which sinks in float-sink sorting and actually aids separation from PP

Weaknesses:

- Limited chemical compatibility with strong essential oils, alcohol-heavy fragrances, and some active cosmetic acids

- Lower service temperature, softening around 70°C, which rules out hot-fill applications

- Less impact resistance than PP at thin wall thicknesses

PET works particularly well for water-based skincare, hair care, and body care formulations where transparency matters and chemical stress is moderate.

PP at a Glance

Polypropylene (PP) is the most versatile of the cosmetic packaging resins. It is also the most-used single polymer in Europe, accounting for the largest share of plastics converter demand. In cosmetics, PP shows up everywhere: caps, closures, jars, tubes, deodorant sticks, lip balms, mascara components, and increasingly in mono-PP dispensing systems and droppers.

Strengths:

- Excellent broad chemical resistance, including for essential oils, fragrances, and active acids

- High service temperature, suitable for hot-fill processes and steam sterilization

- Good fatigue resistance, ideal for flip-top caps, hinges, and pump components

- Lower density (~0.90 g/cm³), which floats in water and separates cleanly from PET in sorting

- Lower material cost than PET in most market conditions

Weaknesses:

- Semi-crystalline structure scatters light, so it is at best translucent, never glass-clear

- Less mature recycling infrastructure: PP collection and sorting yields lag well behind PET, which benefits from established bottle-to-bottle loops

- Food-grade and contact-sensitive rPP supply is limited, which constrains PCR strategy

PP is the obvious answer for any packaging that combines aggressive formulations, mechanical complexity (pumps, flip-top caps, hinges), or hot-fill requirements.

Head-to-Head: The Comparison That Matters

The Cost Picture

At the virgin resin level, PET and PP sit in broadly similar territory in European markets. Both are commodity polymers priced off crude oil derivatives, and the gap between them shifts with capacity cycles, feedstock costs, and import flows from Asia. Through 2025 and into 2026, PP has been well supplied in Europe and prices have stayed subdued, while PET has seen more import competition. Neither material is reliably cheaper in absolute terms across a multi-year horizon.

The real cost story sits in PCR pricing. Food-grade recycled PET carries a persistent premium over virgin PET, and through 2025 the spread between food-grade rPET pellet and virgin PET widened to several hundred euros per tonne. That premium had a visible market effect: rather than push recycled content higher, a number of brands scaled back rPET use toward the mandatory minimum to control cost, which by late 2025 left the market better supplied and narrowed the spread again. Recycled PP carries a smaller absolute premium, but food-contact-grade rPP supply is significantly tighter, which limits how aggressively brands can push PCR content beyond the 10% PPWR floor.

Bottom line on cost: virgin PET and virgin PP are broadly comparable. Once you commit to meaningful food-grade PCR content, PET tends to get more expensive, and that premium has proven structural rather than purely cyclical.

The Supply Chain Risk Most Brands Underestimate

This is where the choice between PET and PP becomes strategic.

PET sits downstream of the beverage industry, which accounts for the large majority of PET bottle consumption. Beverage packaging also carries its own binding recycled-content targets: under the EU Single-Use Plastics Directive, PET beverage bottles must contain at least 25% recycled plastic from 2025, rising to 30% for all plastic beverage bottles from 2030. Those mandatory floors, not voluntary corporate pledges, are now the dominant pull on food-grade rPET. Several large beverage brands have in fact softened or pushed back their voluntary recycled-content goals, but the regulatory minimum still sets a demand floor that competes for the same washed, food-grade recyclate a cosmetic brand would need.

The result: food-grade rPET behaves like a regulated, supply-constrained commodity. Collection and food-grade reprocessing capacity, not consumer demand, set the pace, and forecasters expect the gap between mandated demand and available food-grade supply to sustain a structural premium through at least 2030. For a smaller cosmetic brand, that can mean competing for high-quality rPET against much larger buyers, at premium prices and with less negotiating leverage.

PP's supply chain is different, and in some ways more comfortable for cosmetics. PP demand is spread across automotive, household products, transport packaging, electrical and electronic equipment, construction, and textiles. No single end-market dominates the way beverage dominates PET, so cosmetic packaging is rarely the marginal buyer competing against a much larger industry for the same feedstock.

The flip side: PP's recycling stream is less mature, and food-grade rPP supply is particularly limited. PP also carries its own risks, since propylene feedstock is exposed to crude oil shocks and geopolitical disruption, and virgin PP prices have historically been volatile.

The honest summary:

- PET PCR risk is mostly demand-side: a regulated, beverage-anchored pull on a limited pool of high-quality food-grade recyclate

- PP PCR risk is mostly supply-side: the recycling infrastructure, especially for food-contact grades, is simply less built out

- Virgin material risk is comparable for both, since both are commodity petrochemicals exposed to oil prices, freight, and capacity cycles

For cosmetic brands with ambitious recycled-content targets, PP can offer a more insulated PCR procurement position. Not because rPP is abundant, but because the brand is not bidding against the beverage industry for the same molecule. That advantage rarely shows up on a material specification sheet.

When To Choose PET

PET is the right call when:

- Transparency is part of the product story: visible formula, color cues, premium feel without glass

- The formulation is water-based or mildly emulsified (lotions, toners, shampoos, conditioners)

- The packaging is a relatively simple bottle-and-cap geometry

- You need to hit a 30%+ PCR target with confidence on supply

- Cold-fill processes are sufficient

When To Choose PP

PP is the better fit when:

- The formula is chemically aggressive, with essential oils, fragrances, alcohol-heavy products, or exfoliating acids

- The packaging requires complex mechanical features such as flip-top caps, integrated hinges, dispensing pumps, or droppers

- Hot-fill or sterilization is part of the production process

- You are designing tubes, jars, deodorant sticks, mascara, or lip products

- You want to avoid direct PCR procurement competition with the beverage industry

- Material cost pressure is significant and a 10% PCR target is acceptable

A practical example from our own portfolio: the patented Twin Pack duo-bottle, designed to combine two products (shampoo and conditioner, sun and after-sun, shower gel and scrub) in a single unit, uses HDPE bottles with PP flip-top caps. The system is built around polyolefin chemistry precisely because it has to survive the mechanical and chemical demands of bathroom and travel use.

The Composite Trap

Most "PET bottles" on shelf today are not mono-material. A PET body with a PP cap, a metallized closure, a PVC sleeve, or a multi-material pump is a composite, and under PPWR's design-for-recycling framework, that composite will not earn a top recyclability grade. Going truly mono-material means committing to all components in the same resin family. That includes:

- Bottle and cap in the same polymer

- Pumps and dispensers redesigned in mono-PP or mono-PET versions

- Decoration via in-mould labeling, direct printing, or compatible sleeves

- Avoiding metallized finishes, PET-G overcaps on PET bottles, and dissimilar inserts

This is where most projects stall. The base container is the easy part; the closure system, the pump, and the decoration are where compromises tend to creep back in.

The Bottom Line

Both mono-material PET and mono-material PP are valid answers under the PPWR, but to different questions. PET wins where clarity, water-based formulations, and a mature PCR supply chain are priorities. PP wins where chemical aggressiveness, hot-fill, complex closures, mechanical durability, or insulation from beverage-industry PCR competition dominate the brief.

The strategic decision is rarely "which material is better." It is "which material's tradeoffs fit my product, my formulation, my fill process, my PCR commitments, and my procurement position." Virgin material costs are broadly comparable, so the decisive cost and risk factors live downstream, in PCR pricing and in how exposed your packaging program is to demand from much larger industries. Get that mapping right early in development, and the design-for-recycling work follows naturally. Get it wrong, and the path to a top recyclability grade gets expensive fast.

At Corpack, we work with brands at exactly this decision point, translating formulation requirements, brand positioning, and regulatory targets into the right mono-material construction. Whether the answer is PET, PP, or one of the alternative materials in our portfolio, the principle is the same: the packaging only delivers its sustainability story if every component is part of the same recycling stream.

Looking for help selecting the right mono-material system for your next launch? Get in touch. We have been designing and developing cosmetic packaging in Munich since 1995.